The Brent forward curve is sending one of the strongest signals the oil market has produced in decades — and it’s not subtle.

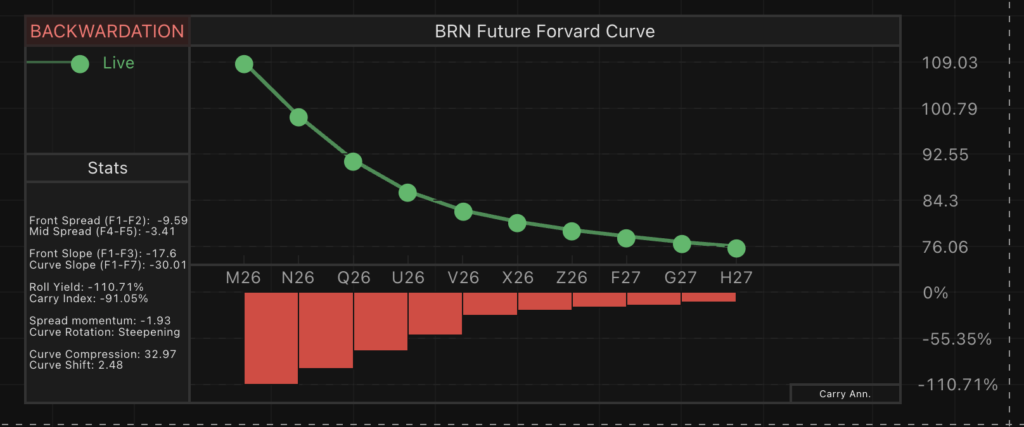

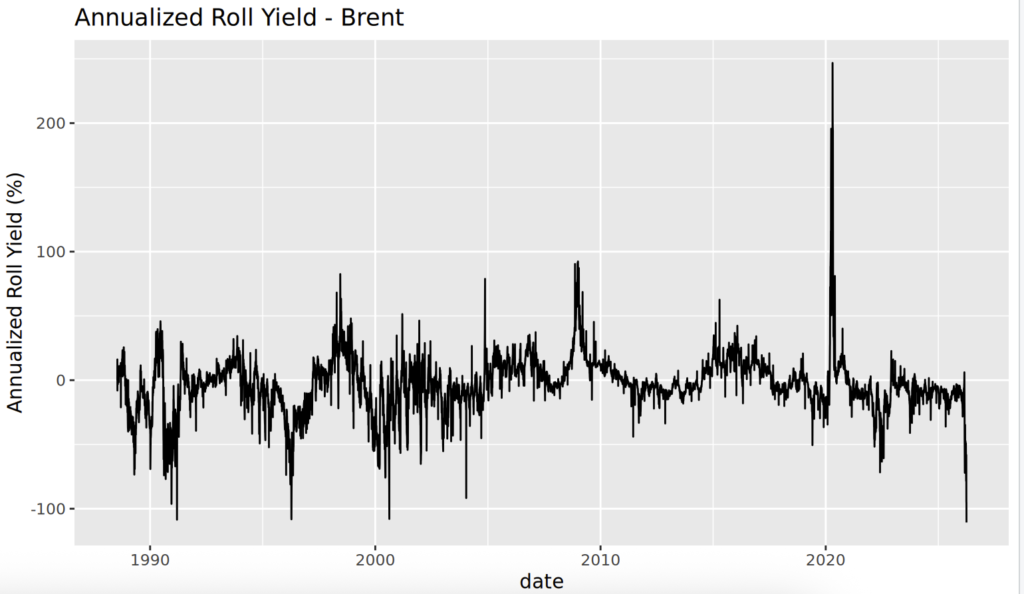

The front of the curve has collapsed relative to deferred contracts, pushing the annualized roll yield between the first and second contract to around -110%. By any historical standard, this is extreme. In fact, comparable readings have only been seen a handful of times — March 1991, April 1996, and August 2000 — and even then, not quite at today’s magnitude.

This is not just backwardation. This is stress.

A Market Paying Almost Anything for “Now”

In commodity markets, backwardation reflects a simple reality:

Immediate supply is more valuable than future supply.

But the current structure goes far beyond normal tightness. A front spread approaching -$10 between the first two contracts implies that market participants are willing to pay a massive premium to secure crude today rather than wait even a few weeks.

That kind of pricing doesn’t emerge gradually. It tends to appear when:

- Physical inventories are tight or rapidly declining

- Supply chains are constrained

- Buyers are forced into the spot market

In short, the system is under pressure.

Why -110% Roll Yield Matters

Roll yield is often an abstract concept — until it isn’t.

At -110% annualized, the cost of holding a long position in front-month Brent futures is enormous. Investors rolling exposure forward are effectively “bleeding” value at a historic rate. This is one of the most punitive environments imaginable for passive long commodity strategies.

But that same dynamic creates the opposite incentive elsewhere:

- Storage becomes unattractive → inventories are drawn down

- Physical holders are rewarded for selling immediately

- The curve self-reinforces tightness in the prompt market

This is how backwardation can accelerate into extreme territory — it actively discourages the very behavior (storage) that would normally stabilize prices.

Rare, But Not Without Precedent

The last times we saw comparable levels of front-end stress were:

- March 1991 — in the aftermath of the Gulf War

- April 1996 — during a period of tightening balances and supply disruptions

- August 2000 — ahead of a broader commodity upcycle

Each episode shared a common feature: acute short-term imbalance, not necessarily a long-term shortage.

That distinction matters.

The forward curve is not forecasting where oil prices will be in a year — it is reflecting the urgency of supply today.

What the Curve Is Really Saying

At its core, the Brent curve is delivering a very clear message:

The issue is not future supply — it is the availability of barrels right now.

This time, the driver is not abstract tightness or gradual imbalance. It is a clear geopolitical shock. The escalation of conflict involving Iran and the disruption of flows through the Strait of Hormuz — a critical artery for global oil exports — has created an immediate and tangible supply risk.

When a meaningful share of global seaborne crude is suddenly at risk, the market reacts where it matters most: the front of the curve.

The result is mechanical:

- Buyers rush to secure prompt cargoes

- Physical availability tightens sharply

- Near-term prices surge relative to deferred barrels

Regardless of how long the disruption lasts, the impact is already visible:

The market is scrambling for immediate supply, and pricing crude today at a significant premium to crude tomorrow.

Opportunity, Risk, and What Comes Next

Extreme backwardation creates sharp asymmetries across the market:

Winners

- Physical traders with access to crude

- Producers selling into elevated spot prices

- Those positioned for continued tightness

Losers

- Passive long investors rolling futures

- Storage operators

- Anyone relying on stable curve structure

However, history also offers a warning.

These conditions rarely persist indefinitely. Once supply constraints ease — whether through increased production, demand softening, or logistical normalization — the front of the curve can reprice violently.

In other words, the same steep structure that signals scarcity today can unwind just as quickly.

Final Thought

A triple-digit negative roll yield is not just a market signal — it’s a market alarm.

The Brent curve is no longer quietly indicating tightness; it is aggressively pricing immediacy. Whether this reflects genuine scarcity or a temporary dislocation will determine the next phase of the oil market.

But one thing is clear:

Right now, the market doesn’t just want oil — it needs it now.