If you’ve ever looked at the Silver futures chain and noticed something strange, you’re not alone.

April contracts are listed. They’re tradable. They haven’t expired.

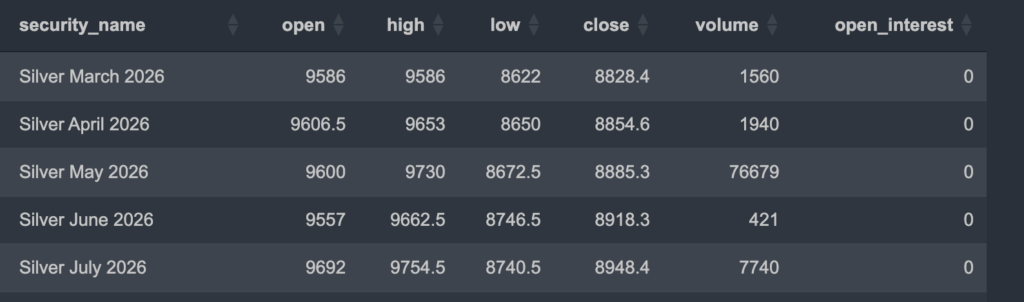

And yet, most of the volume and open interest sit in May and even July.

So what’s going on?

Why does Silver futures volume seem to skip April?

The answer isn’t random. It’s structural.

Silver Futures Don’t Treat Every Month Equally

Silver futures trade on COMEX, part of the CME Group.

And while contracts may be listed for many calendar months, the exchange defines specific major delivery months for Silver:

- March

- May

- July

- September

- December

These are the primary contract months around which the entire liquidity structure is built.

Other months — such as April — are known as serial months.

They are official.

They are tradable.

But they are not primary delivery cycles.

That distinction matters more than most traders realize.

What Is a Serial Month?

A serial month is an exchange-listed contract month that falls between the major delivery months.

For Silver futures:

- April sits between March and May.

- It exists.

- But it is not part of the main institutional delivery rhythm.

Serial months typically have:

- Lower open interest

- Thinner order books

- Wider bid-ask spreads

- Minimal institutional participation

They function more as optional trading months rather than liquidity hubs.

Why Volume Clusters in May and July Instead

There are four structural reasons Silver futures volume skips April.

1️⃣ Liquidity Attracts Liquidity

Large participants — hedge funds, banks, commodity trading advisors — need depth.

They prefer:

- Tight spreads

- Minimal slippage

- Large order execution capability

That liquidity already exists in major months like May and July.

So capital naturally concentrates there.

Liquidity is self-reinforcing.

2️⃣ Institutional Hedging Aligns With Major Delivery Months

Commercial hedgers — refiners, producers, industrial users — operate on standardized cycles.

Major delivery months are where:

- Physical delivery infrastructure is optimized

- Warehouse logistics are standardized

- Clearing processes are streamlined

Serial months rarely attract significant physical positioning.

So the “real economy” flow skips April as well.

3️⃣ The Roll Cycle Skips April

As a major contract month approaches expiration — for example, March — funds begin rolling forward.

They typically roll:

- March → May

- Later May → July

They do not roll March → April → May.

Why?

Because April lacks sufficient depth to absorb large systematic rolls.

Open interest doesn’t disappear — it migrates.

And it migrates into the next major liquid month.

4️⃣ Market Structure Is Designed Around Major Months

This pattern isn’t accidental.

Commodity futures markets historically evolved around:

- Seasonal production cycles

- Industrial consumption schedules

- Quarterly financial reporting cycles

The major delivery months reflect that structure.

Serial months exist for flexibility — not dominance.

Open Interest Migration: What You’re Actually Seeing

When you notice April sitting with low open interest while May builds aggressively, you’re observing liquidity migration, not market inefficiency.

Here’s what typically happens:

- As March nears expiration, its open interest declines.

- Traders roll forward.

- Most of that positioning concentrates in May.

- Some longer-dated positioning extends into July.

April never becomes the focal point because institutional size bypasses it entirely.

This creates the illusion that April is being ignored — when in reality it was never meant to be the primary liquidity hub.

Why This Matters for Traders

Understanding contract structure has real trading implications.

If you trade lower-liquidity serial months:

- Spreads can widen significantly.

- Slippage increases.

- Technical signals may be less reliable.

- Large stops may move price disproportionately.

For most active traders, using the front major liquid month is the safest choice.

For example:

- After March begins rolling off, May becomes the active contract.

- Later, July takes over.

This is why charting platforms often auto-roll to the next major month rather than the nearest calendar month.

This Isn’t Unique to Silver

Silver just makes it obvious.

Many commodity futures contracts — especially metals and energy — have:

- Defined major delivery months

- Secondary serial months

- Liquidity is concentrated in specific cycles

It’s part of the futures market microstructure.

Once you understand that, volume patterns stop looking mysterious.

They start looking mechanical.

The Bottom Line

April Silver futures aren’t broken.

They aren’t ignored.

They aren’t unofficial.

They’re simply a serial month in a market designed around major delivery cycles.

Liquidity clusters where institutions operate — and institutions operate in the primary contract months.

So when you see volume building in May and July while April sits quietly, you’re not witnessing irrational behavior.

You’re witnessing structure.

And in futures markets, structure explains almost everything.